Toggle each shareholder between SELL / ROLL OVER / AGAINST / UNDECIDED. Scheme requires ≥75% by value of votes cast + majority by number of holders.

Real-time engagement status — saved locally. Update as outreach progresses.

🔴 Asset disposal update: Glasgow SOLD · Edinburgh SOLD (franchise) · Berlin CLOSED · Holland Park IN EXCLUSIVITY (near gone) · Elephant & Castle confirmed for disposal (ICP removes from list) · York for sale · Brighton operating on sale & leaseback.

Larry confirmed HSBC debt full repayment plan from disposal proceeds → equity becomes debt-free. Conversion priority confirmed: Passeig de Gràcia (Barcelona) → Madrid → Lisbon → Athens.

Brief Tuvi Keinan (Brown Rudnick) and Huntsmead/2V on Larry's positive signal before coffee. Do NOT table a fixed p/share before seeing management information.

Use these as private call notes, objection logs, and open Q&A per stakeholder. Auto-saved to your browser.

Key employees by region. Excludes shareholders and board NEDs. Retention priority and photo status shown. Click any card to open their intelligence dossier.

{id}.jpg in photos/ folder

| Fee Type | Rate | Amount | When |

|---|---|---|---|

| Arrangement / Promote | 2% of capital raised | £17,000 | On close |

| Development Management | Fixed | £100,000 | Hotel opening (deferred) |

| Asset Management | 1.5% gross revenue p.a. | £6.7K → £26K | Yr 1 → Yr 3 |

| Exit / Option Advisory | 1.5% of asset value | TBD | On option exercise/sale |

| Fee Type | Rate | Amount (5yr) | Annual |

|---|---|---|---|

| Base Management Fee | 2% of revenue | €1,420,583 | €215K → €454K |

| Asset Management | 0.75% of equity p.a. | €378,778 | €94,695 / yr |

| Incentive Fee | 8% of GOP | Incl. in mgt fee | — |

| GP Promote | 20% above hurdle | €3,291,413 | On exit (Yr 4) |

| Fee Type | Rate | Amount | When |

|---|---|---|---|

| Transaction Fee | 3% of project cost | €152,778 | On close |

| Base Management | 1%–3% revenue (scaling) | €33.7K → €95.1K | Yr 1 → Yr 3 |

| Incentive Fee | 6%–8% of GOP | Incl. in mgt total | — |

| Combined (Yr 3) | — | €120,197 | Annual at stabilisation |

| Fee Type | Rate | Illustrative | When |

|---|---|---|---|

| Management Fee | 1.5% p.a. committed capital | €300K–€750K / yr | Annual (Estonian OÜ) |

| Carried Interest (GP) | 20% above 8% pref return | 20% of profits above hurdle | On exit / distributions |

| Rolling SH Enhanced Carry | 25% (vs. 20% standard) | Above hurdle for rolling SHs | On exit |

| Project | Total Cost | Equity Need | Proj. Return | ICP Fees (Est.) | 1st Revenue |

|---|---|---|---|---|---|

| 🇬🇧 Shoreditch | £850K | £850K | 15–20% CoC | ~£168K (3yr) | End May 2026 |

| 🇫🇷 Paris | €25.6M | €12.6M | 12–15% IRR | ~€5.1M (5yr) | Q1 2028 |

| 🇮🇹 Milan | €5.2M | €2.1M | 8–12% IRR | ~€440K (4yr) | Q3 2027 |

| 🏴 Silo | €50–100M | €20–50M | 21–26% IRR | 1.5%+carry | Post-acq. |

| Advisor | Role | Carry % | Scope | Rationale |

|---|---|---|---|---|

| Huntsmead Partners | Lead Advisor & LP Placement | 2–3% | All Deals | Primary capital raiser; carry aligns quality of LP introductions with long-term fund performance. |

| Brown Rudnick (Keinan / Hodge) | Legal — Takeover Panel & Structuring | 1–1.5% | Silo Only | Deferred legal fees + carry. Generator €776M precedent. Panel process is binary — need committed counsel. |

| Shore Capital | NOMAD & Fairness Opinion | 0.5–1% | Silo Only | NOMAD + Lipman relationship holder. Carry secures loyalty through scheme. Critical for Board recommendation. |

| Stanhope Capital | Debt Coordination & Institutional | 0.5–1% | Silo Only | Debt placement linked to carry; reduces upfront fees. Natural alignment — carry irrelevant if debt doesn't close. |

| Reserved (unallocated) | Future advisors / management | 1–2% | TBD | For operating partners, management retention post-close, or additional advisors. GP discretion with LPAC notification. |

| Exit Scenario | Equity In | Equity Out | Profit Above Hurdle | Total Carry (20%) | ICP Core (13%) | Advisor Pool (7%) |

|---|---|---|---|---|---|---|

| 🟡 Base Case (2.0×) | €30M | €60M | €18M | €3.6M | €2.34M | €1.26M |

| 🟠 Target Case (2.6×) | €30M | €78M | €36M | €7.2M | €4.68M | €2.52M |

| 🟢 Bull Case (3.2×) | €30M | €96M | €54M | €10.8M | €7.02M | €3.78M |

Advisors compensated purely on fees-for-service have no economic incentive to stay engaged through deal stress. When Pyrrho demands a higher price, when Bredbury's CLN creates a veto risk, when debt markets wobble — fee-based advisors can walk away. Carry-aligned advisors cannot.

The advisor carry pool creates a self-reinforcing alignment loop: Huntsmead is incentivised to bring quality LPs (not just any capital), Brown Rudnick is motivated to navigate the Takeover Panel flawlessly (their carry depends on deal completion), and Shore Capital stays loyal through the scheme process (their carry depends on Board recommendation). Singer CM is separately aligned via success-based transaction fees (2.7%/1.75% — they only get paid on completion).

The cost is modest. At a 2.6× exit, 7% of carry = €2.5M spread across carry participants. The alternative — losing a €78M exit because an advisor disengaged at a critical moment — is catastrophically more expensive. This is insurance priced as incentive.

Comp Set: Generator (916 beds, €24-48/bed) · JO&JOE Gentilly (485 beds, Accor-backed, €25-50) · St Christopher's (350 beds, €21-42) · Les Piaules (162 beds) · Le Montclair 18ème

Pricing: Lume target £35-52/bed (≈€41-60) — above Generator dorms but below private rooms. No capsule hotel brand exists in Paris = first-mover advantage.

Comp Set: Ostello Bello Grande (~300 beds, €31-71) · Ostello Bello Duomo (~150 beds) · Combo Milano (Navigli, €25-45) · Ostelzzz (capsule, €30-55)

Pricing: Lume target £35-50/bed (≈€41-58). Only one capsule competitor (Ostelzzz, lower spec). Ostello Bello dominates — Lume must differentiate on product.

Comp Set: Generator BCN (702 beds, €16-48/bed) · TOC · Sant Jordi · Onefam · Equity Point

Lume Thesis: Capsule pods at £38-52/bed — 3-4× Generator dorm rate but below private rooms (€68-219). Wellness + tech stack as differentiator.

Comp Set: The Hat (220 beds, €35-51/bed) · 2060 Newton (211 rooms, spa, €30-55/bed) · Generator (200+ beds) · TOC · Bastardo

PRICING REVISED UP: Original £21-23 was underpriced vs. comp set. New target: £30-38/bed (≈€35-44) — in line with The Hat.

Competitive Intelligence

LIFESTYLE HOSTEL MARKET · PRIMARY COMPS · DEAL BENCHMARKS

SafeStay PLC trades at a significant discount to private market comps. Generator's Brookfield exit at €776M (~14× EBITDA) in May 2025 is the definitive benchmark — SafeStay currently trades at ~6–8× EBITDA on AIM. This gap is the take-private opportunity.

Design-led "affordable luxury." Queensgate → Brookfield (€450M→€776M in 8 years = 1.72×). ICP implication: SafeStay at 14× EBITDA exit = £40–55M equity value. Direct rebranding comparator for Lume.

Listed NASDAQ Oct 2022 then collapsed. ICP implication: Validates take-private thesis — public markets structurally mis-price lifestyle hostel operators. SafeStay's AIM discount is institutional, not fundamental.

Amsterdam + Copenhagen. Full automation via RFID + app. Minimal staff model. ICP implication: CityHub achieves 40%+ higher RevPAR than SafeStay through tech. This is the benchmark for Lume 2.0 AI revenue management upside.

Rome-based. Invel Real Estate JV 2025 for Southern Europe rollout. ICP implication: Confirms Mediterranean institutional appetite. SafeStay Italy/Spain unencumbered assets (debt repayment lever) overlap with YSquare target cities.

| Operator | Properties | EV Multiple | ADR | Ownership |

|---|---|---|---|---|

| Generator | 17 | ~14× EBITDA | £55–70 | Brookfield (2025) |

| Selina | 175+ | Public (distressed) | £30–45 | NASDAQ (SLNA) |

| CityHub | 5 | ~12–15× est. | £65–80 | Private |

| YellowSquare | 3 | ~12× est. | €40–55 | Invel JV (2025) |

| SafeStay (AIM) | 23 | ~6–8× AIM | £30–40 | ICP TARGET ← GAP |

Larry Lipman — Approach Intel

CHAIRMAN · FOUNDER · KEY SWING VOTE · 13.6% OF SSTY

"Larry, you built something extraordinary — a brand that proved premium hostels work at scale. Your vision was right. Now we bring the capital, the brand execution, and the AI platform to take it where you always believed it could go. Lume is SafeStay 2.0 — your legacy, amplified."

- Chairman & Founder, SafeStay PLC (2011–present)

- Managing Director, Safeland PLC (property, 30+ yrs)

- Known for iconic UK property locations (Edinburgh, Kensington)

- Strong relationships in UK property and finance circles

- Conservative, relationship-driven; dislikes surprises

- 13.6% of SafeStay PLC (via Safeland entities)

- Chairman — controls board narrative & timing

- Key to unlocking irrevocable undertaking

- s.135 rollover candidate: ~£1.33M at offer price

- Warm route: Stanhope Capital (→ Shore → David Coaten)

Aggregate themes from employee reviews — internal use only. Use to frame execution narrative, NOT to criticise Larry personally.

- High staff turnover / workload pressure

- Management communication inconsistency

- Pay levels below market benchmarks

- Limited career progression pathways

- Revenue management manually driven, not tech-enabled

- Fun, international team culture

- Diverse traveller community appreciated

- Iconic central locations (genuine asset)

- Vision and brand coherence (Larry's core gift)

- Property portfolio — real hard assets

ICP Frame: The execution gaps are not a personal failure — they are a resourcing and technology deficit. Larry's vision was correct. The platform (Lume 2.0 + AI) is what was missing. ICP brings the capital + systems to close that gap. Lead with respect for what he built → acknowledge what the business needs next → offer him a stake in the future.

Lume 2.0 — AI Platform Vision

POST-ACQUISITION TECHNOLOGY ROADMAP · NOT FOR EXTERNAL DISTRIBUTION

SafeStay is a portfolio of blue-chip urban locations running on 2010s-era operations.

Lume 2.0 replaces the operating system with AI-native hospitality —

yielding +£8–12 RevPAR/night and -15% cost/available room.

Dynamic pricing updated every 30 minutes across all 20 properties using ML demand signals, local event data, competitor rate intelligence, and weather triggers.

App-first check-in, AI concierge (city recommendations, F&B upsell, activity booking), keyless room access, and personalised on-property experience. Staff-to-guest ratio cut by ~25%.

Automated generation of property photography (Imagen 4 Ultra), social content (Veo 2.0 cinematic video), and multilingual marketing copy — eliminating £150–200K/yr in agency spend per city.

Real-time dashboard aggregating: occupancy by property, RevPAR vs budget, maintenance alerts, demand forecasts (14-day), guest satisfaction scores. Replaces manual GM reporting.

Day 1–6m

6m–2yr

2yr–5yr

Rolling Shareholder Tax Efficiency

s.135 TCGA 1992 · PAPER-FOR-PAPER EXCHANGE · LEADING ARGUMENT FOR LARRY & ANSON

The data tells the story: SafeStay shares at 15p — down ~33% from the 26p 52-week high. The public market has delivered its verdict on execution under Larry Lipman. This is not a reflection on Larry's vision — he was right to build the estate. The hostel tourism thesis is proven. But without the tech platform and institutional capital, the execution gap closes the door on public market recovery. ICP's offer: new management, Lume 2.0 AI, 3-year turnaround — at a premium to today's 15p (offer price TBD). This is not a hostile takeover. It's a rescue with respect for what Larry built, and a rollover that gives him a seat at the table for the upside.

- DAHL Bidco acquires ≥25% of ordinary voting shares of SafeStay

- Consideration is wholly or partly in new shares of DAHL/ICP

- Exchange is bona fide commercial (not tax avoidance scheme)

- Not a pre-arranged sale scheme under HMRC clearances

- No CGT on the exchange itself (disposal deferred)

- Base cost of new ICP shares = original SafeStay cost

- CGT deferral lasts until eventual exit of ICP shares

- Lena Hodge + Brown Rudnick advise on HMRC advance clearance

Core Infill Capital Partners team leading the Project Silo take-private acquisition of SafeStay PLC. All communications under strict NDA and Project Silo confidentiality protocols.

Shore Capital acts as SafeStay's NOMAD and Broker. These contacts are our primary engagement route for the Panel process and Board approach. Gateway to Larry Lipman (Chairman, ~13.6%).

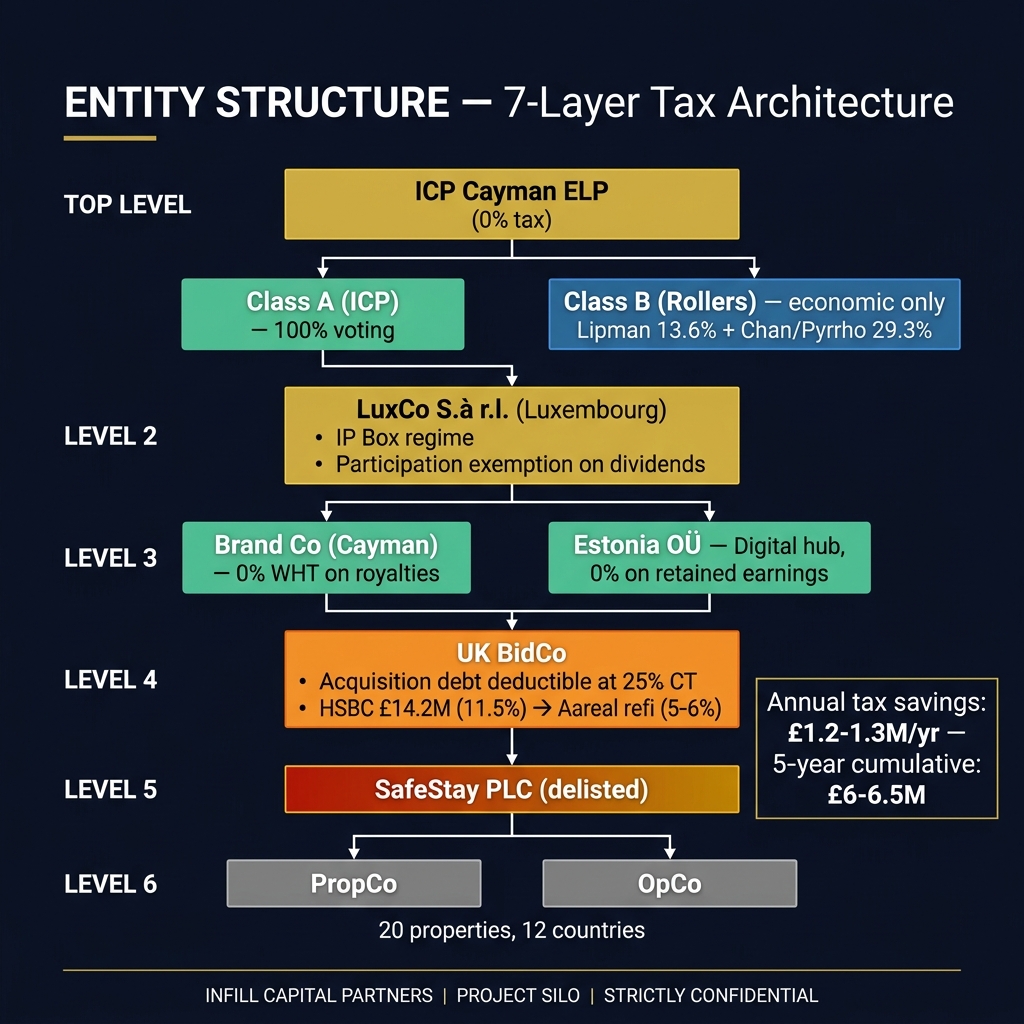

Institutional-grade Cayman ELP co-investment structure with Luxembourg S.à.r.l. BidCo. Designed for LP tax efficiency (s.135 TCGA rollover), Takeover Code compliance, and Lume platform scalability post-close.

⚠️ CONFLICT OF INTEREST: Larry Lipman as Chairman of SafeStay PLC personally holds (via Safeland / Safeland Holdings 2008 Ltd) the freehold interest in the E&C property — while SafeStay PLC (the entity he chairs) is the leaseholder paying rent to his own vehicle. This creates a material conflict: Lipman benefits from freehold disposal proceeds while SafeStay shareholders bear the ongoing lease liability with no freehold value on the balance sheet. This arrangement, combined with the Edinburgh and Brighton disposals, systematically strips freehold value from the group to Lipman-controlled entities — a governance concern for any incoming acquirer and a potential Rule 21 issue if disposals accelerate during the offer period.

| Role | Firm | Key Contact | Status |

|---|---|---|---|

| UK Takeover Counsel | Brown Rudnick LLP | Lena Hodge / Tuvi Keinan | ✅ Engaged — SOW signing |

| Financial Adviser (Rule 3) | Singer Capital Markets | Rick Thompson / James Todd | ✅ Engaged |

| Certain Funds Verification | Morgan Stanley | — | ✅ Engaged |

| Placement Agent | Huntsmead | Barnaby Joy / Piers Talalla | ✅ Engaged |

| Senior Debt | Multiple lender options | Via existing relationships | ✅ Engaged |

| Luxembourg CSP | Hawksford Luxembourg | Amaury Mairlot / Claude Crauser / Sinan Sar | 🟡 Onboarding |

| Luxembourg Counsel | LAB Partners | Benoit Kelecom | 🟡 Intro call this week |

| Cayman Counsel (GP+ELP) | Harneys (preferred) | — | 🟡 Awaiting response |

| Lead LP | Hill Hardman / Hadi Irvani | US Family Office | ✅ Committed |

| Operating Advisor | Josh Wyatt | Generator / Equinox pedigree | ✅ Engaged |

Core transaction documents for Project Silo. Click any document to open in the reader.

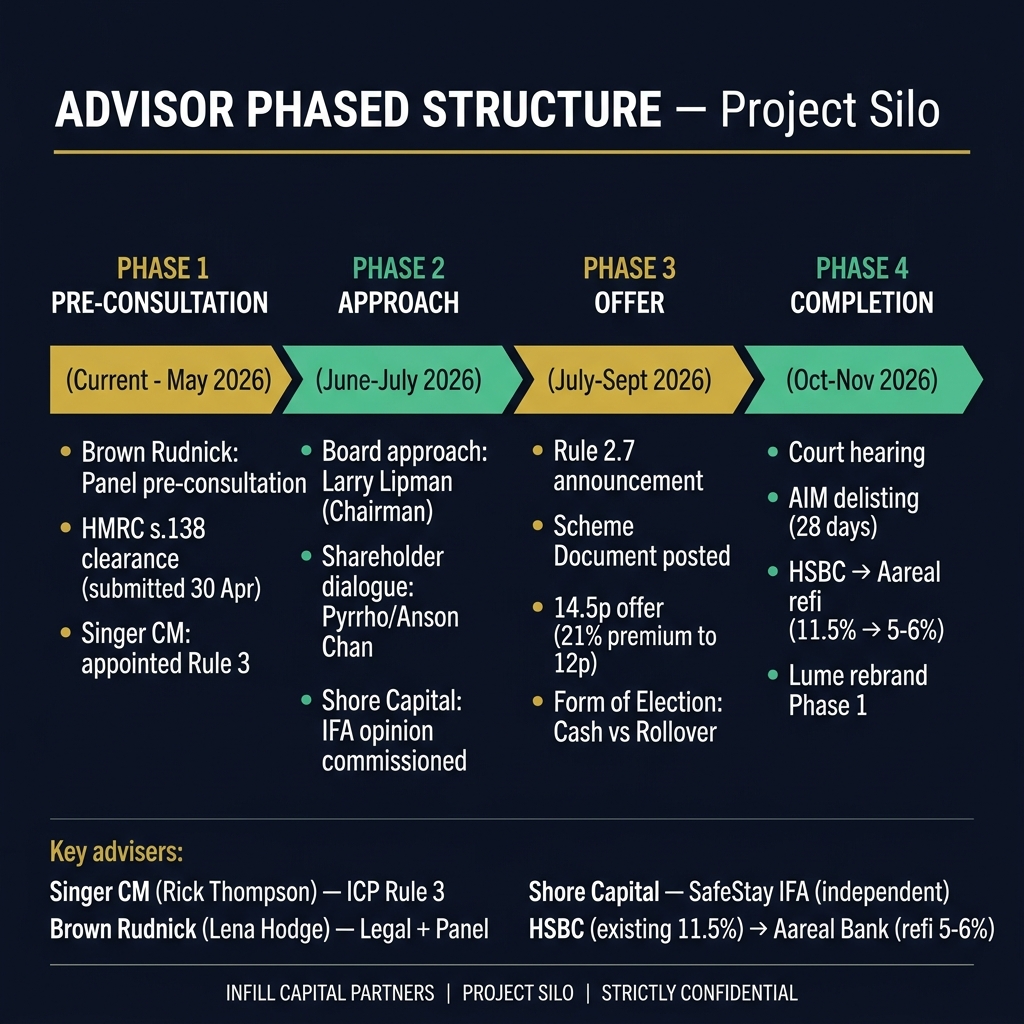

Last updated: May 5, 2026 · Singer Capital Markets appointed as Rule 3 Financial Adviser

(1) Singer CM engagement letter execution · (2) Brown Rudnick — Scheme document drafting · (3) HMRC s.138 clearance application · (4) Chan family intro via Erik Fok · (5) Hawksford — LuxCo S.à.r.l. incorporation · (6) Charge 005 review — change-of-control clause

Prepared for: Shore Capital (NOMAD/Broker) | Brown Rudnick (ICP Counsel) | Internal use only

Offer: TBD per share | premium to undisturbed | Rollover option available to all shareholders

For Larry: "Safestore flew when it got institutional backing. BizSpace flew when it got institutional backing. SafeStay is the same story — and you defer all CGT to the exit you control."

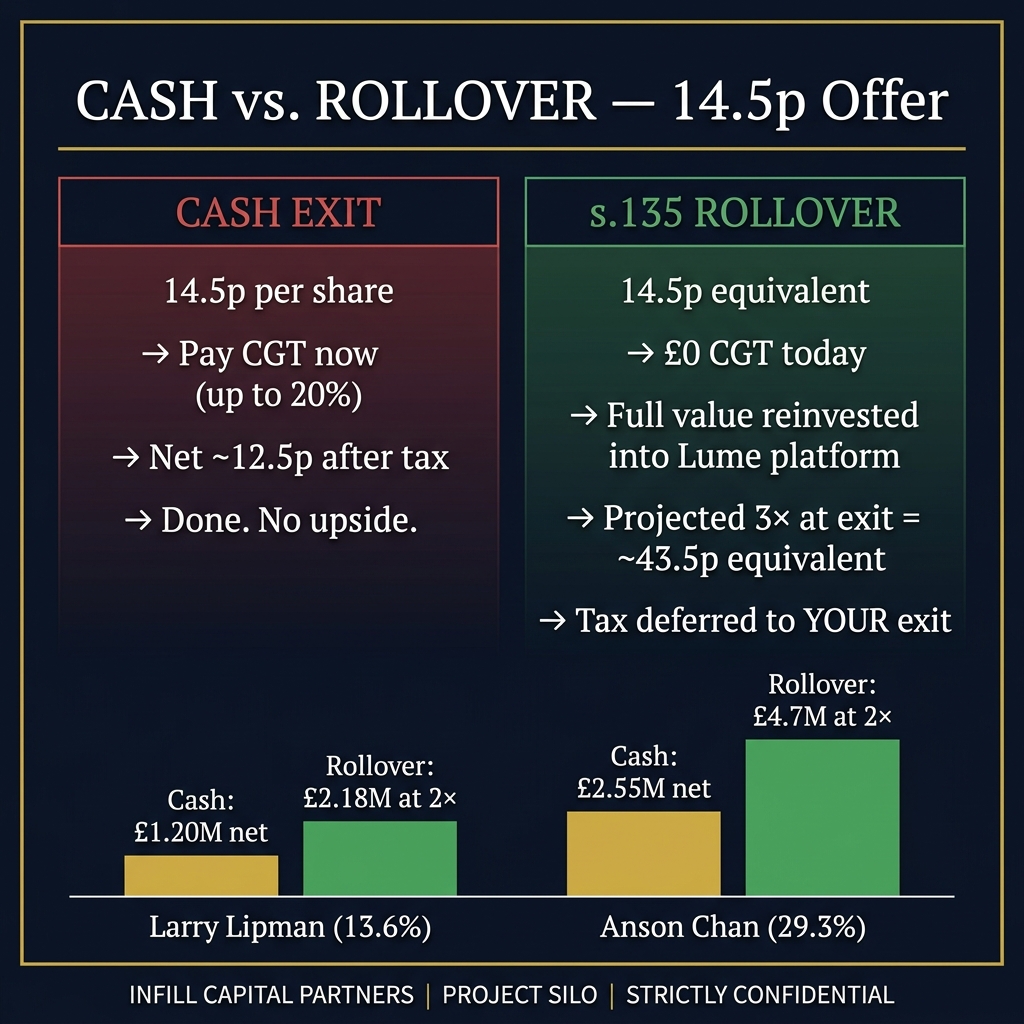

For Anson/Pyrrho: "You spotted value here before anyone else. The s.135 structure means you didn't sell at 15p — you reinvested your original thesis at the right capitalisation point. The £8.6M rollover outcome vs £4.4M cash exit net speaks for itself."

For all shareholders: "The cash price is [offer price]. Your net rollover value at ICP's 3× projected exit is significantly higher — with CGT deferred until you decide to sell."

| Shareholder | ❌ Cash Exit Today | ✅ s.135 Rollover | Rollover Upside |

|---|---|---|---|

| Larry Lipman (~£2.3M proceeds) | Net ~£2.14M After CGT ~20% |

£0 CGT today Full £2.3M reinvested |

~£3.9M at 3× +£1.76M vs cash exit |

| Anson Chan (~£4.9M proceeds) | Net ~£4.4M After CGT, UK res complication |

£0 CGT today Full £4.9M reinvested |

~£8.6M at 3× +£4.2M vs cash exit |

| All others (18p cash option) | 18p per share | Optional rollover on identical terms |

Per HMRC clearance |

□ Offer rollover available to ALL shareholders (equal terms)

□ Disclosed in Rule 2.7 firm intention announcement

□ Independent adviser confirmation (Shore Capital)

□ Panel consultation via Brown Rudnick / Lena Hodge

□ Timeline: 4-6 weeks from application

□ UK HoldCo must issue ordinary shares

□ Commercial purpose test satisfied

□ BADR eligibility confirmation (Larry)